{kind=link}

By SETH JOSEPH

That is half 3 of Seth’s sequence about Epic that has generated a lot curiosity and somewhat controversy and we’re blissful to host it on THCB. Half 1 and Half 2 have been revealed on Forbes earlier this yr.

In keeping with individuals within the room, Judy Faulkner’s imaginative and prescient on stage at Epic’s 2022 Person Group Assembly was epic, within the grandest sense of the phrase.

The corporate, which had grown as a unified scientific and billing EHR system, was now laying out a roadmap through which it could be the digital entrance door for all issues shopper dealing with. An enormous panoply of capabilities together with, in response to Epic’s personal subsequent documentation, buyer relationship administration, supplier finders and on-line scheduling, on-line check-in, affected person monetary expertise, and lots of others.

Core to enabling all of this was shifting how sufferers work together with MyChart, the patient-facing software that permits people to entry their well being data.

Traditionally, every MyChart account was ‘tethered’ between a person and a hospital system and represented a easy portal for the person to view her data. If a person had been seen at a number of totally different hospital programs, then she would have a number of separate MyChart “situations”, or totally separate accounts and logins.

Now, Epic would ‘sew collectively’ the well being data and information from totally different hospitals on behalf of the person in advancing what colloquially has been known as Epic’s ‘nationwide MyChart technique’, and allow sturdy new performance, creating compelling community results between shoppers and hospitals.

There have been just a few issues with Epic’s technique: first, many purchasers weren’t asking Epic to develop these capabilities; second, there have been startups and incumbents already offering many of those capabilities; and third, the corporate was in a race with a federal company, which was pushing for open requirements and entry that threatened Epic’s plans.

However for a corporation that had slowly and steadily develop into the dominant well being know-how participant, whose employees conferences for a interval ended half-jokingly on a slide with the phrases “World Domination” on them, these issues have been all fixable.

The Promise Of Client Empowerment Instruments

As fashionable historical past has demonstrated again and again, the power to personal or management the patron entry level for know-how could be a strategic benefit. Apple’s modern product designs, person expertise and tight ecosystem allow it to extract 30% of app developer revenues looking for to succeed in Apple’s customers. Google’s dominance in search has positioned it to be the entryway to the web for billions of shoppers no matter their final vacation spot, leading to extraordinary income progress and profitability.

In healthcare, the power to meaningfully have interaction shoppers by means of know-how has lengthy held promise of fixing intractable issues, whereas additionally probably positioning the agency that figures out how to take action as a brand new locus of energy, equally as Apple and Google above. Triaging care choices for shoppers, navigating them to decrease value providers, facilitating funds, and offering fashionable comfort choices are just some of the a whole bunch of use instances that consumer-facing know-how holds.

Key questions dealing with the companies looking for to seek out healthcare’s holy grail are how finest to do that and the place to start out, as shopper habits and sentiment towards healthcare has confirmed difficult for tech corporations to determine.

For example, tech giants Microsoft and Google had each positioned important bets on ushering a brand new period of shopper empowerment within the late-2000s, with Microsoft HealthVault and Google Well being. Referred to as affected person well being data (PHR), the 2 corporations sought to allow shoppers to entry, mixture, retailer and probably share their well being data.

On reflection, Microsoft and Google’s efforts have been maybe a bit too early, as each initiatives have been shut down within the early 2010s, earlier than an ecosystem of well being know-how adoption, connectivity and capabilities that would have feasibly supported their imaginative and prescient. And earlier than shoppers had a compelling motive to alter their very own use of know-how to have interaction of their healthcare.

By 2022, nonetheless, the ecosystem had arrived. After the EHR Incentive program, greater than 90% of docs and hospitals had EHRs. The Covid-19 pandemic drove fast adoption of telehealth by each physicians and shoppers. Roughly $100 billion in enterprise capital had flowed into well being know-how innovation. New value transparency insurance policies have been shedding daylight into previously opaque and labyrinthine contracting practices. The twenty first Century Cures Act put tooth into driving interoperability, introducing info blocking as a civil penalty with million greenback fines. One trade group revealed a report titled “Unbundling Epic: How The EHR Market Is Being Disrupted.” This writer proclaimed The EHR Is Lifeless.

If the EHR was useless or being disrupted, then each EHR firm wanted a survival plan.

Epic’s Worry And Unfair Benefit

In keeping with one hospital government, it was this backdrop that involved Epic’s management: with a fast inflow of recent gamers and a shifting steadiness of energy, Epic may be relegated to “simply being the pipes” whereas others capitalized on new alternatives. Given the corporate’s inflexible perception – confirmed right time and time once more – that it alone would ship the most effective outcomes for its clients and shoppers, Epic thought such an end result could be a catastrophe.

To fight this threat, Epic by mid-2022 had a brand new technique with MyChart and community results on the coronary heart of it.

Prior up to now, Epic had allowed its hospital clients to construct their very own consumer-facing purposes on prime of the MyChart chassis, or to herald third-party options to take a seat on prime of and combine with MyChart. To help this, Epic offered software program growth kits (SDKs) to clients, and allowed integration choices to 3rd get together distributors.

Supporting this innovation was vital to some Epic clients. Specifically, bigger well being programs (sometimes these with extra assets and class) seen their consumer-facing capabilities as an vital approach to differentiate themselves out there.

The brand new technique entailed driving adoption and utilization of MyChart (already the most effective recognized patient-facing software within the nation), growing new consumer-facing capabilities and pushing hospitals to make use of these, and capturing shoppers as their most popular software of selection.

Briefly, Epic sought to broaden its sphere of affect, from a place of market dominance over one sector of healthcare (hospital programs) into one other: shoppers.

To take action, Epic crafted a coherent coverage and set of ways designed to steer hospitals to get on board with its imaginative and prescient, muscle out rivals, and affect regulation in an effort to obtain its ends.

Epic’s Ways Leverage Its Strengths, However Elevate Essential Anti Aggressive Questions

As beforehand reported, Epic arguably has a monopoly place with its inpatient EHR amongst multi-hospital well being programs and tutorial medical facilities. Since that reporting, Epic has continued to achieve market share; its software program is now used at hospitals accounting for 51% of all beds nationwide. As a number of hospital executives have put it in conversations, Epic is operating away with the EHR market.

The EHR could also be generally considered a scientific software, however it could be extra correct to consider it because the hospital’s working system. The distinction will be vital: an software offers workflow capabilities to realize a particular goal, whereas an working system acts as an interface between the person and {hardware} that controls the foundations by which purposes operate and the assets it has entry to.

Take into account that whereas docs and clinicians use the EHR as an software, it appears totally different from the hospital enterprise perspective: the EHR is the default system that its most extremely skilled, paid and busiest employees work together with daily, rendering it the one most vital system; the information entered by clinicians shops affected person data and related info that’s used for mission-critical functions together with billing, reporting, and audit capabilities; and accordingly, it’s the system which just about each different software should accordingly combine with (and never vice versa).

Because the hospital’s ‘working system’, Epic’s nationwide MyChart technique begins out with pure built-in benefits versus patient-facing know-how rivals, together with:

- MyChart footprint: The federal Significant Use Program required hospitals to make use of EHRs that offered a affected person portal. In the present day, Epic’s MyChart boasts between 190M and 300M shopper accounts, an unimaginable early benefit given the rising utilization of private well being data.

- Key shopper infrastructure and integration: A affected person portal is of restricted utility to a shopper. However one which begins out built-in with the supplier system, permitting single-sign on, scheduling, messaging, telehealth and associated methods the patron might wish to work together together with her supplier, can present substantial worth.

- Hospital relationships and belief: The worth of having the ability to roll out new capabilities to current clients representing 60% of all well being system spend at a single occasion (on this case, the 2022 Epic person group assembly) can’t be overstated. Nor can the years and, oftentimes, a long time of trusted relationships that Epic has cultivated with its clients.

In keeping with hospital and trade executives, Epic is within the technique of pulling all of those levers. And whereas some rivals might complain about these built-in benefits, the truth is that Epic is dominant within the inpatient EHR marketplace for good motive, and it’s a sensible technique to leverage its current strengths throughout product, capabilities and relationships to advance its nationwide MyChart imaginative and prescient.

Nevertheless, a few of Epic’s different ways, although they might show to be extremely efficient, increase questions. Listed here are 4 particularly:

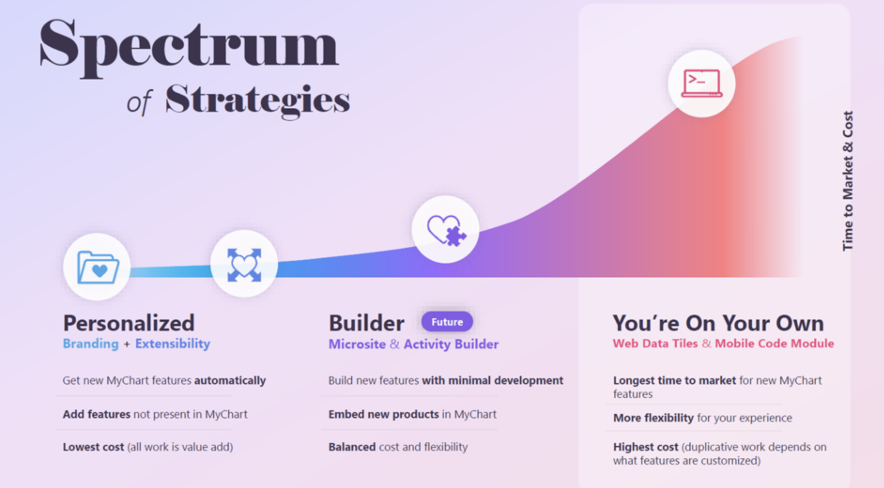

1. “You’re On Your Personal”: A yoyo can imply a silly or incompetent particular person, a time period Epic has determined to use to a few of its clients. On the firm’s 2022 person group assembly, Judy Faulkner launched the time period “you’re by yourself” (yoyo) to discuss with Epic hospital clients who needed to take care of their very own digital front-door technique. Shifting from its historic stance of being agnostic as as to if hospitals used solely Epic’s MyChart or most popular to develop their very own consumer-facing technique that built-in with MyChart, Epic made clear it needed hospitals to forgo their very own technique and get on board with a extra Epic-controlled model of MyChart. In step with this want are Epic supplies that clearly display function divergence for purchasers adopting its most popular ‘Personalised’ model of MyChart versus function discrimination for these ‘yoyo’ clients.

2. Altering Price Construction For ‘Yoyos’ and Elevating Costs To Steer to MyChart: In keeping with executives from a number of programs who discovered themselves being known as ‘yoyos’, Epic additionally subsequently and unilaterally has tried to alter its payment construction for know-how and help prices associated to MyChart. Traditionally, Epic charged a flat payment to help hospitals who both constructed their very own consumer-facing purposes that built-in with MyChart or partnered with industrial distributors for a similar function. After it introduced its nationwide MyChart technique, nonetheless, Epic started notifying ‘yoyo’ clients that it was shifting to a brand new pricing construction based mostly on the variety of shoppers the hospital served. A number of hospital executives talked about that this is able to enhance the related MyChart charges by a number of thousand p.c, from tens of hundreds of {dollars} yearly to tens of millions; the choice was to keep away from these incremental charges by abandoning their very own consumer-facing methods and opting in to Epic’s nationwide MyChart technique.

In response to questions on these modifications, an Epic spokesperson famous that MyChart charges themselves had not modified since 1999. With respect to know-how and help prices, the spokesperson famous, “With ‘You’re On Your Personal,’ clients can select to license extra instruments that enable their builders to embed elements of MyChart into their very own buyer purposes.”

3. Eliminating Preexisting Interoperability Entry: Epic had traditionally supported its ‘yoyo’ clients, partially, by offering MyChart integration and interoperability assets to distributors that these clients select to work with for consumer-facing purposes. With the introduction of its nationwide MyChart technique, nonetheless, Epic has begun limiting entry to these assets. In some instances, Epic has allegedly let slip to some distributors, together with these they’ve labored with for years collaboratively, that they’re now rivals, and that Epic could be “sunsetting” (eliminating) current interoperability assets and that the distributors wouldn’t have entry to future iterations of the identical assets.

Based mostly on a evaluate of an Epic e mail response to a person requesting the standing of beforehand accessible assets, what Epic seems to be doing in some instances is withdrawing software programming interfaces (APIs) from its open.epic website, and shifting these to its ‘Vendor Companies’ program. An preliminary problem for any vendor looking for to combine with Epic is that APIs in its Vendor Companies program aren’t revealed or discoverable. A vendor looking for to use to this program should first fill out and submit a questionnaire, however Epic offers no steering on what the factors for inclusion or exclusion are, nor the way it determines what API assets can be accessible or to whom. This observe exposes Epic to claims that it could be selecting winners and losers.

4. Delaying Requirements (Which Could Drive MyChart Adoption): The Nationwide Institute of Requirements and Know-how is a department of the U.S. Division of Commerce. Its IAL2 commonplace is meant to permit for distant id proofing, which is important to enabling a future through which people can request and entry their very own medical data from current well being info networks that suppliers use routinely. Enabling people to make use of digital purposes of their option to entry their data is a precedence for ASTP/ONC, the federal company chargeable for selling interoperability. Epic introduced in August that they might help this functionality, however with a twist: the corporate helps the IAL2 commonplace to permit people to find the place they’ve acquired care, however to not request and retrieve their data.

Some trade cynics have privately claimed that Epic’s stance will lead to people nonetheless needing to have an current or create a brand new MyChart account, which can enhance charges Epic expenses to hospitals (as MyChart charges are volume-based) and enhance lock-in of Epic’s ecosystem.

An Epic spokesperson flatly denies this, noting “Use of MyChart strictly for authorization to share information by way of OAuth 2.0 [another technical standard for identity authorization] doesn’t increment any MyChart subscription counter, doesn’t lead to any extra expenses to our clients, and is unlikely to draw new customers to MyChart.”

————–

Individually, every tactic might help a legit enterprise function. For example, whereas “yoyo” may appear a crude time period, it’s according to Epic’s usually playful and inventive naming conventions. Altering its payment construction might replicate Epic making a course correction to a expensive approach of supporting clients, as an Epic spokesperson instructed. And as trade insider and analyst Brendan Keeler has famous, Epic is a chief amongst EHRs with regards to enabling particular person entry providers, so it’s onerous to critique.

Taken altogether, nonetheless, the collective ways are sufficient to have some trade insiders and buyers involved that they’re anticompetitive.

Is Epic Unfairly Urgent its Excessive Floor Benefit?

Having grown organically since 1979 and solely previously decade changing into the chief in EHR, it’s doable that Epic’s insular tradition blinds it to its personal market power and affect in adjoining markets.

In that case, it could behoove Epic to replicate on points involving fellow tech giants who leveraged dominant market positions in a single enterprise to unfairly and illegally benefit themselves when dealing with know-how shifts and altering shopper habits. Most related stands out as the Microsoft lawsuit, through which Microsoft was discovered to be illegally using its dominant place as an working system to exclude rivals within the rising net browser market. And the newer case in opposition to Google, through which Choose Mehta discovered the corporate acknowledged the ability of default placement and distribution to illegally safe and broaden its place.

In Epic’s case, the corporate holds a dominant place because the hospital’s working system. By eradicating current APIs and interoperability assets to consumer-facing corporations and altering payment constructions, it’s making it extra cumbersome and costly for hospitals to pick various patient-facing applied sciences, making MyChart the default path ahead. One end result is the notion that its ways are exclusionary in nature and foreclose on innovation in an rising market. One other end result, additionally problematic for Epic, is diminished shopper selection and elevated direct prices (to hospitals) and oblique prices (to rivals and shoppers).

But, Epic arguably doesn’t must make use of these ways to win. MyChart appears well-positioned to finish up as essentially the most sturdy, seamless and compelling ecosystem for shoppers on account of Epic’s trusted relationships with hospitals, dominant market share and current (and rising) community results.

In the interim and absent any pressure majeure stopping Epic from executing its plan, it appears like Epic’s shopper technique is prone to lead to community results that much more firmly entrench the corporate’s place and set up one other locus of energy. If profitable, Epic might discover itself ready like Apple, with the power to extract a considerable income share from any developer looking for to entry shoppers for whom Epic could be the default “digital entrance door”.

Should you work in Verona Wisconsin, it is a good factor. Perhaps too, in the event you’re a shopper.

Seth Joseph is the Founder and Managing Director of Summit Well being Advisors